In the world of business, your accounts are more than just a record of spending; they are your company’s resume. Whether you are applying for an export credit line or seeking an MSME loan, the strength of your financial statements determines your success.

1. The Accounting Equation: Your Financial Balance

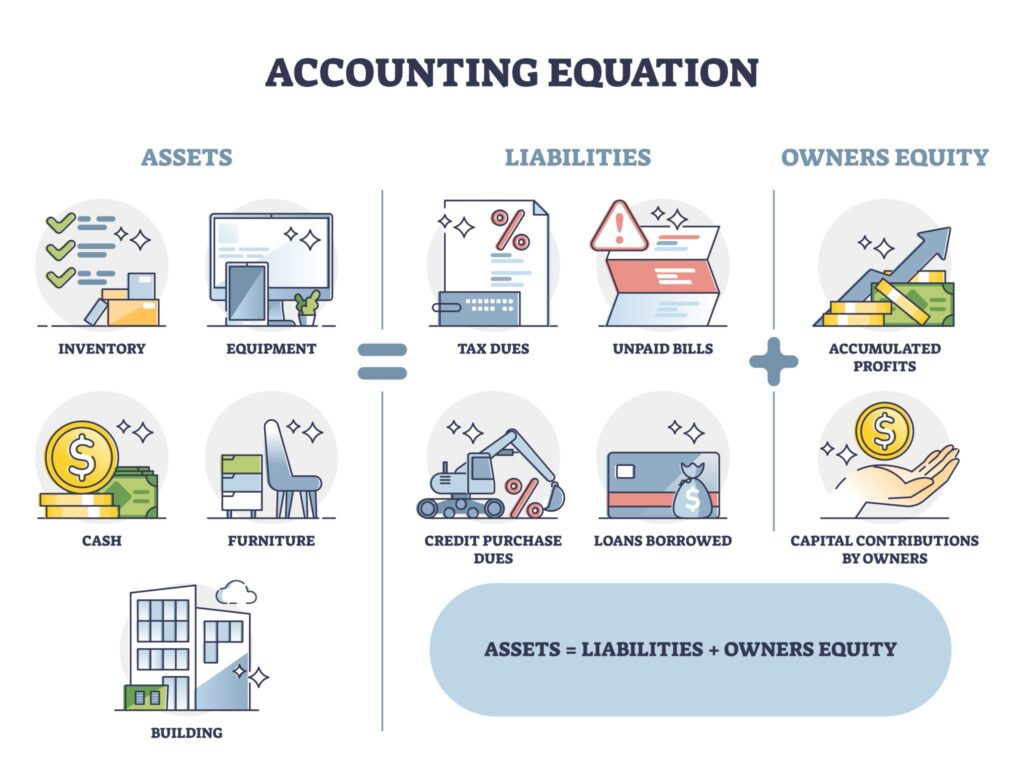

The entire world of accounting rests on one simple, non-negotiable formula. If this doesn’t balance, your financial story has a “plot hole.”

Assets = Liabilities + Equity

- Assets: Resources you control (Cash, Machinery, Inventory, Accounts Receivable).

- Liabilities: Your obligations (Bank loans, Trade payables, Taxes).

- Equity: The “residual interest” what is left for the owners after all debts are settled.

2. The Three Pillars of Financial Reporting

To a banker or an investor, these three documents are the “holy trinity” of your business health:

| Statement | What it Tells You | The Goal |

| Balance Sheet | A snapshot of your position at a specific date. | Shows Solvency (Can you pay long-term debts?) |

| Profit & Loss (P&L) | Your income and expenses over a period. | Shows Profitability (Is the business model working?) |

| Cash Flow Statement | Where the actual cash went (not just paper profit). | Shows Liquidity (Can you pay your bills tomorrow?) |

3. Understanding Debits and Credits

Think of the General Ledger as a scale. Every transaction must be recorded in at least two places to keep that scale balanced this is called Double-Entry Bookkeeping.

- Debit (Dr): Generally increases an asset or expense account.

- Credit (Cr): Generally increases a liability, equity, or revenue account.

Example: If you take a bank loan of $10,000, you Debit your Cash account (Asset increases) and Credit your Loan account (Liability increases).

4. Accrual vs. Cash Accounting: Why it Matters for Funding

Most small businesses start with Cash Accounting (recording money when it actually hits the bank). However, for manufacturing and exports, Accrual Accounting is the standard.

- Accrual Accounting records income when it is earned and expenses when they are incurred.

- Why? It gives a truer picture of your business’s future obligations and expected income, which is exactly what lenders look for during credit assessment.

5. Why “Good Books” are Your Best Funding Strategy

Clean accounting isn’t just for tax compliance; it’s a strategic tool:

- Accurate Working Capital Assessment: You can’t ask for the right loan amount if you don’t know your operating cycle.

- CIBIL & Credit Health: Regular reconciliation prevents missed payments that hurt your score.

- Audit Readiness: Being “bank-ready” means having your documents organized before you need the money.

The “Exporter’s Edge”: Accounting for Global Trade

For a manufacturer selling locally, accounting is straightforward. But for an exporter, your books need to handle a few extra variables. If these aren’t managed correctly, they can eat into your margins or, worse, make you look “high-risk” to a bank.

1. Managing Currency Fluctuations (Forex)

When you invoice a client in USD but your expenses are in INR or AED, the value of that invoice changes every day.

- Realized Gain/Loss: The difference in value when the payment actually hits your bank.

- Unrealized Gain/Loss: The “on-paper” change in value for an open invoice at the end of the month.

- Pro Tip: Accurate bookkeeping of these fluctuations shows lenders you are managing Exchange Rate Risk effectively.

2. Accounting for Letters of Credit (LC)

An LC is a commitment, but how do you record it?

- Contingent Liability: While an LC isn’t a “debt” yet, it is a commitment of your bank’s credit line.

- The Trap: If you don’t track your LC limits in your internal accounts, you might over-leverage yourself and face a sudden liquidity crunch.

3. Inventory and Work-in-Progress (WIP)

For manufacturers, accounting isn’t just about “Stock In/Stock Out.”

- WIP Accounting: You must track the value of raw materials currently on the factory floor.

- Funding Impact: Banks provide Pre-shipment Finance (Packing Credit) based on the value of your raw materials and WIP. If your accounting doesn’t clearly show these values, you’ll likely get a lower loan amount than you deserve.

4. Duty Drawbacks and Subsidies

As an exporter, government incentives are part of your revenue.

- Don’t just “mix” these with sales. Record them as Other Operating Income.

- Keeping these separate helps you analyze your true “product-only” profitability versus your “incentive-aided” profit.

Conclusion: Don’t Just Record, Analyze

Accounting is the bridge between your hard work in the factory and the capital you need to grow. When your basics are solid, your business becomes “Fundable.”

Expert Checklist for Your Next Audit:

- [ ] Are my Forex gains/losses clearly categorized?

- [ ] Is my Work-in-Progress (WIP) valued accurately for my bank’s drawing power?

- [ ] Are my LC and BG limits reconciled with my bank statement?

I really like how you framed the three financial statements as different parts of a business’s story. It’s a great reminder that profitability doesn’t always reflect cash flow, and both need to be clear when presenting to lenders or investors. This perspective really helps business owners see the bigger picture in their accounting.

Thank You:)