One of the biggest pain points for MSMEs today is delayed customer payments. You’ve delivered the goods, raised the invoice, but now you’re stuck waiting 30, 60, even 90 days to receive your money. That’s where Invoice Financing steps in as a game-changer.

What is Invoice Financing?

It’s a short-term borrowing solution where businesses raise funds against unpaid invoices.

Instead of waiting for your customer to pay, you get up to 80–90% of the invoice value upfront from a financier. Once your customer pays, the financier deducts their fees and returns the balance to you.

Invoice financing helps businesses improve cash flow, pay employees and suppliers, and reinvest in operations and growth earlier than they could if they had to wait until their customers paid their balances in full. Businesses pay a percentage of the invoice amount to the lender as a fee for borrowing the money. Invoice financing can solve problems associated with customers taking a long time to pay as well as difficulties obtaining other types of business credit.

It is also known as Account receivble Financing or Receivable Financing.

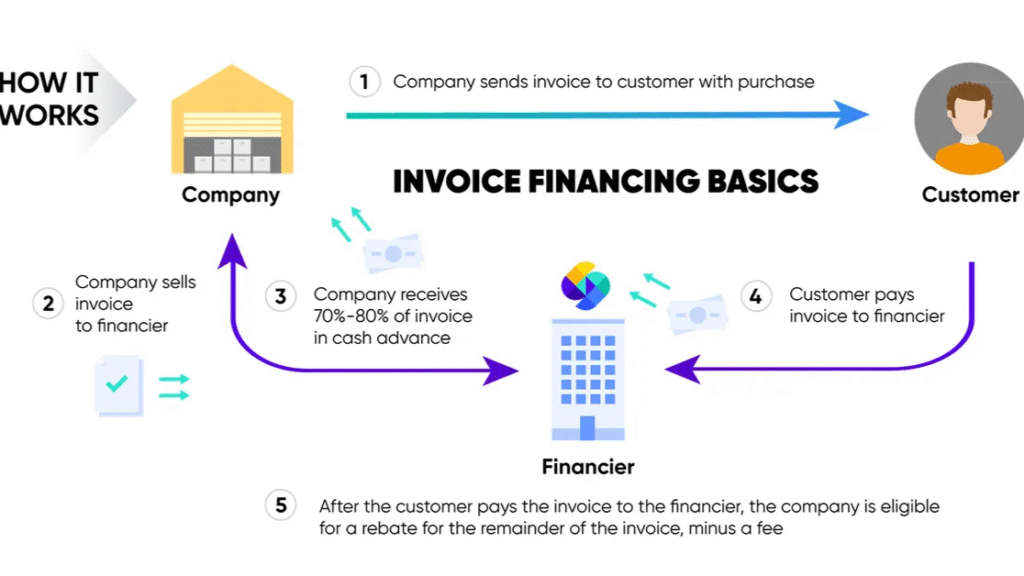

How It Works – Step by Step

- You supply goods/services to a customer and raise an invoice.

- You submit this invoice to a lender or platform.

- They verify the invoice and disburse funds (usually within 48–72 hours).

- Once the customer pays, the lender settles the balance.

Types of Invoice Financing

- Invoice Discounting – You retain customer relationship; lender stays in the background.

- Invoice Factoring – Lender takes control of collections; visible to customer.

Why It’s a Lifeline for MSMEs

- Improves cash flow instantly

- No collateral required (invoice acts as security)

- Access to immidiate working capital.

- Funds grow with sales – more invoices, more liquidity

- Reduced debt burden.

- Quick disbursal – solves seasonal or temporary crunches

- Flexibility-It allows businesses to manage cash flow more effectively and react to opportunities or challenges.

What to Watch Out For

- Hidden charges or processing fees

- Over-dependence on receivables-based funding

- Customer creditworthiness matters – not just yours

- Timely customer payments are crucial

Invoice Financing From the Lender’s Perspective

Invoice financing benefits lenders because, unlike extending a line of credit, which may be unsecured and leave little recourse if the business does not repay what it borrows, invoices act as collateral for invoice financing. The lender also limits its risk by not advancing 100% of the invoice amount to the borrowing business. Invoice financing does not eliminate all risk, though, since the customer might never pay the invoice. This would result in a difficult and expensive collections process involving both the bank and the business doing invoice financing with the bank.

Risks

- Fees and Interest: Invoice financing is not free; it involves fees and interest charges, which can be high.

- Non-Payment Risk:While the lender may cover some bad debt, the business still faces the risk of non-payment from their customer.

- Impact on Customer Relations: If the business uses factoring (where the customer is notified about the invoice financing), it may impact customer relationships.

- Over-Leveraging: Businesses need to carefully consider their debt load and avoid over-leveraging their financial resources.

Real MSME Scenario

Let’s say an MSME supplies ₹10 lakhs worth of material to a reputed buyer with 60-day credit. Using invoice financing, they can immediately receive ₹8–9 lakhs, fund payroll, raw materials, or a new order, and keep the business engine running.

Who Uses Invoice Financing?

Invoice financing is used by businesses across various sectors, including construction, retail, transportation, and consumer goods. It’s particularly attractive to small and medium-sized businesses (SMEs) that may find it difficult to obtain traditional bank loans or need a quick source of funds to manage cash flow.

Final Thought

In a world where cash flow is king, invoice financing ensures you’re not stuck waiting while your business slows down. Invoice financing is a valuable tool for businesses to improve cash flow and access funding, but it requires careful consideration of the associated fees, risks, and impact on customer relationships.

It’s not debt—it’s unlocking what’s already yours.

Key Takeaways

- Invoice financing allows a business to use its unpaid invoices as collateral for financing.

- A company may use invoice financing to improve cash flow for operational needs or speed up expansion and investment plans.

- Invoice financing can be structured so that the business’ customer is unaware that their invoice has been financed or it can be explicitly managed by the lender.

Want to explore invoice financing for your business?

Let’s talk.