MSME lending is stepping into a new era where data is the new collateral and algorithms are the new underwriters. But this future isn’t just about fancy models rather it’s about speed, trust, explainability, and real-world outcomes: more approvals for good borrowers, fewer shocks for lenders, and stronger, more resilient small businesses. Here’s what’s changing, why it matters, and how to act. Whether you’re a banker, a fintech, or an MSME owner this is must know for all of us.

1) What’s Really Changing?

- From balance-sheet-first to cashflow-first: Lenders are shifting from static documents to live cashflow signals (bank statements, GST/VAT trails, POS, e-commerce, payroll) to see ability and willingness to pay in near-real time.

- From CIBIL/AECB-only to alternative data: Bureau scores still matter, but they’re increasingly complemented by behavioral and transactional data.

- From manual underwriting to AI-assisted decisions: Humans still decide, but AI now gathers, cleans, and scores risk with far greater consistency and speed.

- From one-size-fits-all to hyper-tailored credit: Products designed around a borrower’s cash cycle (seasonality, invoice terms, platform sales, export timelines) instead of blunt limits and tenors.

- From opaque to explainable: Regulations and common sense both demand why a decision was taken hence explainable AI (XAI), model monitoring, and consented data-sharing frameworks.

- From days/weeks to minutes: Straight-through processing (STP) with eKYC, eSign, and automated document reading.

2) The New Data Advantage: What Lenders Will Use?

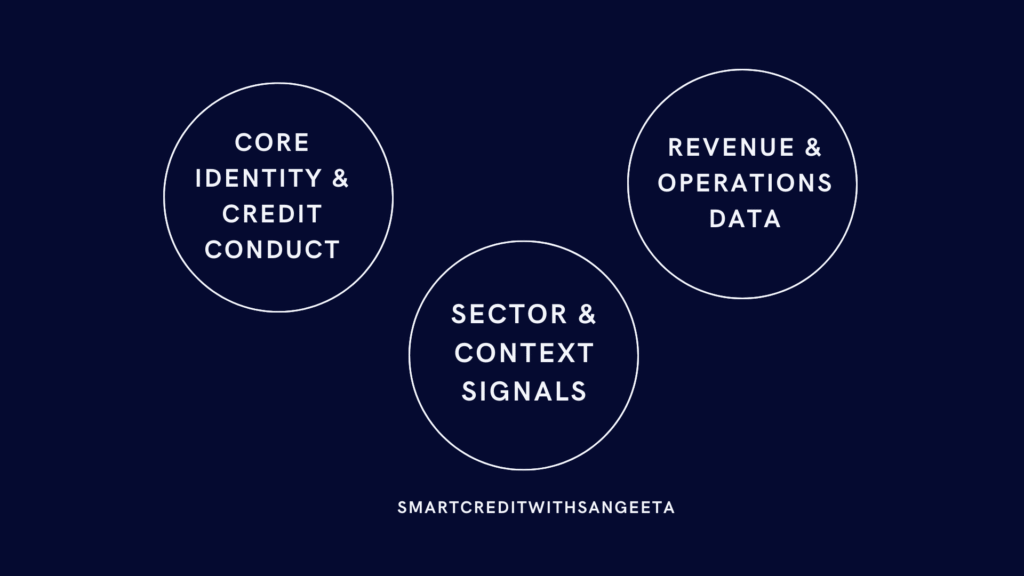

Think of data in three rings:

A. Core identity & credit conduct

- KYC & registrations: Udyam/Trade license, company registry lookups, PAN/Emirates ID, etc.

- Credit bureaus: India (CIBIL/Equifax/Experian/CRIF), UAE (AECB) for repayment history, delinquencies, and exposure.

- Bank statements: 6–24 months for inflow patterns, EMI behavior, minimum balances, bounced instruments.

B. Revenue & operations data (cashflow spine)

- Tax trails: GST/VAT filings (tax paid, returns filed on time, revenue trends, buyer–supplier concentration).

- Sales rails: POS/e-commerce marketplace data, payment gateways, UPI/QR collections, card settlement files.

- Accounts receivable: Invoice ages, buyer ratings, dispute frequency, discounts, and chargebacks.

- Payroll & vendor payments: Salary regularity, seasonality in working capital, vendor concentration risk.

- Inventory signals: Purchase orders, stock turns, shrinkage/out-of-stock events (from basic ERP or even spreadsheet logs).

C. Sector & context signals

- Macro & micro: Commodity price trends, festival/seasonality patterns, monsoon/heat-wave impact for agri-linked MSMEs, export lane risks, logistics disruptions.

- Location intelligence: Pin-code/area business density, footfall, crime, flood risk, last-mile logistics reliability.

For MSMEs: If you want better terms, start making this data clean, consistent, and shareable with consent. Your future “collateral” is your data credibility.

3) What AI Actually Does?

AI in lending is no longer a single score but it’s a decision system with five parts:

- Data ingestion & quality control

- OCR/IDP to extract fields from bank PDFs, invoices, KYC docs

- Entity resolution (is “Sharma Trading Co.” the same as “Sharma Tradg.”?)

- Anomaly detection (duplicate invoices, fabricated sales spikes, round-tripping)

- Feature engineering

- Cashflow features (net inflows, volatility, seasonality, cushion days)

- Conduct features (average days past due, limit utilization, bounce patterns)

- Concentration features (Top-5 buyers/vendors share)

- Scenario tags (festival spikes, export cycle longer tenor)

- Risk & affordability models

- Default risk, possible loss, and exposure

- Affordability calculators (safe EMI as % of net monthly cashflow)

- Early-warning systems (EWS) predicting stress 30–90 days ahead

- Decision policy & pricing

- Rules + ML: minimum bureau cutoffs, blacklists/whitelists, sector caps

- Risk-based pricing and limit setting, with explainability for each decision

- Post-sanction monitoring

- Transactional surveillance (soft triggers vs hard stoppers)

- Dynamic limit management (seasonal top-ups)

- Collections prioritization (which accounts to call, when, with what message)

Key mindset: AI doesn’t replace the credit officer; it amplifies them—cleaner inputs, consistent scoring, faster decisions, better portfolio health.

4) Embedded Finance & “Credit at the Workflow”

Credit is moving to where business actually happens:

- Within marketplaces & ERPs: Seller gets a working capital offer right inside the platform they use to manage orders or inventory.

- Within payments & POS: As your QR and card collections grow, pre-approved revolving limits rise automatically.

- Within invoicing software: Raise an invoice, instantly get a financing offer based on buyer rating and historical payment behavior.

Why this matters: It slashes acquisition costs, reduces fraud (because transaction data is native), and improves turnaround time (TAT). For MSMEs, it means less paperwork, faster cash but also a need to keep digital records clean.

5) Consent, Privacy, and Explainability (Non-negotiable)

Modern MSME lending relies on consented data sharing and clear decision reasons:

- Consent rails: Only access data that the borrower explicitly allows; show what’s being pulled and for how long.

- Data minimization: Collect what you need— no more.

- Explainable AI: Provide the borrower with intelligible reasons for approval/decline and what to improve (e.g., “High bounce rate last 6 months” rather than “Model says no”).

- Fairness checks: Monitor for bias across gender, location, income proxies; document mitigation steps.

- Model governance: Versioning, challenger models, backtesting, periodic audits, adverse-action logs.

For lenders, this is risk management and brand-building. For MSMEs, it’s dignity and clarity.

6) What Good Looks Like?

A. Lender Playbook: 12-Month Data & AI Roadmap

Quarter 1 – Data foundation

- Map your “decision-critical” data; instrument reliable ingestion from bank statements, GST/VAT, POS/e-com.

- Implement data quality rules (completeness, consistency, duplicates).

- Build a borrower 360° schema (identity, conduct, cashflow, sector tags).

Quarter 2 – Scoring & policy

- Launch an explainable affordability model (cashflow-based EMI capacity).

- Pilot risk-based pricing with clear guardrails.

- Put an EWS with 3–5 simple, validated triggers (e.g., 2+ bounces, 25% drop in collections, inventory spike without matching sales).

Quarter 3 – Embedded & STP

- Integrate with one partner platform (ERP/POS/marketplace) for embedded journeys.

- Automate KYC, bank statement parsing, income estimation; push for same-day sanctions on clean files.

- Add a model monitoring dashboard (stability, drift, fairness) for compliance.

Quarter 4 – Scale & feedback

- Roll out a “decision reason” summary with every outcome.

- Build collections intelligence (contact strategy by risk bucket).

- Start champion–challenger experiments (new features, sector calibrations).

B. MSME Playbook: How to Become a “Bankability Magnet™”

- Clean your money trail: Use one primary current account for business inflows; avoid cash detours; keep vendor/customer payments through traceable rails.

- File on time—always: GST/VAT returns, TDS, AES—timeliness is a strong signal of reliability.

- Tame bounces: Keep buffer balances; set standing instructions; monitor auto-debits.

- Show your cycle: Maintain simple monthly MIS—sales, collections, payables, stock. Even a clean spreadsheet is gold.

- Diversify concentration: If top 1–2 buyers are >50% of revenue, proactively add new accounts (and show those POs).

- Narrative matters: Prepare a 1-page business note: model, seasonality, key customers, risks and mitigations, ask (amount, tenor, use of funds), and your skin in the game.

- Consent confidently: Share data knowingly; ask lenders how they’ll use it and what will improve your eligibility next time.

7) Product Trends You’ll See More Often

- Cashflow-backed working capital: Flexible limits that breathe with your collections.

- Revenue-based finance: Pay a % of daily/weekly sales; tenor flexes with volume.

- Invoice & PO financing 2.0: Real-time buyer risk mapping and programmatic limits.

- Asset-light collateral models: Combining behavioral data with smaller security to unlock first-time credit.

- Green & transition finance: Preferential terms for energy upgrades and waste-to-value processes, backed by measurable outcomes.

8) Risk, But Smarter: What to Watch Out For

- Data drift and model rot: Market changes break yesterday’s assumptions, so monitor and recalibrate.

- Synthetic identities & deepfake KYC: Use liveness checks, device fingerprinting, and cross-source corroboration.

- Overfitting to a platform: If all your data comes from one marketplace, your risk is tied to that marketplace just diversify inputs.

- Silent seasonality stress: Great Diwali sales don’t mean January repayments will be smooth, price and structure for the troughs.

- Ethical red lines: No dark patterns, no opaque denials. Long-term trust beats short-term disbursal spikes.

9) A Simple, Explainable Cashflow Score

When I design credit flows for MSMEs, I like a 5-pillar score:

- Revenue Stability (25%) – trend, volatility, seasonality, buyer concentration.

- Collections Quality (25%) – bounce rate, average collection period, chargebacks.

- Expense Discipline (20%) – payroll timeliness, rent/utilities regularity, vendor repayment cadence.

- Liquidity Cushion (15%) – average balance days, overdraft usage, emergency buffer.

- Compliance Behavior (15%) – tax filing timeliness, variance flags, bureau conduct.

Output the score and the “why”: “Approved ₹18L at 16% for 18 months. Reasons: steady quarterly growth, low bounce rate, two months cash buffer. Improve: reduce Top-2 buyer concentration (61%) to <45% for better pricing.”

10) For India & UAE Readers

- India: Expect deeper use of GST + bank data for cashflow underwriting, stronger Account Aggregator-style consented data sharing, and more embedded credit via POS/UPI apps and e-commerce ERPs.

- UAE: AECB scores remain foundational; expect faster adoption of POS/e-commerce data and payroll files (WPS) in underwriting, plus continued digitization of KYC and eSign flows in banks and fintech partnerships.

11) What Borrowers Can Do This Week

- Switch to single primary current account for business inflows.

- Start a Monthly Business Snapshot (one-page MIS): sales, collections, payables, stock, EMI calendar.

- Set auto-reminders for tax filings and EMIs; avoid last-minute scrambles.

- Clean up invoice hygiene: correct GST/VAT numbers, consistent item descriptions, buyer names.

- Document seasonality & order pipeline for the next 3–6 months to show lenders your forward visibility.

12) What Lenders Can Pilot This Quarter

- 90-day fast lane for repeat clean customers using bank + GST/VAT data; target sanction <24 hours.

- Early Warning Lightboard: simple dashboard of top 10 at-risk accounts by cashflow anomalies, not just days-past-due.

- Collections intelligence: contact high-risk borrowers before due date when signals turn amber.

- Decision-notes to borrowers: one-screen explanation and next steps to improve eligibility.

13) The Human Core: Why This Future Matters

AI and data can unlock credit where traditional collateral can’t. For the kirana that digitized collections, the home-based manufacturer selling on marketplaces, the export unit with long receivable cycles—smart, ethical lending means growth without guesswork. For lenders, it means scale with control. For communities, it means jobs and resilience.

The future is not “man vs machine.” It’s humans using better instruments with consent, clarity, and compassion.

Bonus from me: Borrower Readiness Checklist (Save/Share)

- Primary business bank account for all inflows

- Zero EMI/tax delays in the past 6 months

- Clean GST/VAT filing history

- Monthly MIS (sales, collections, payables, stock)

- Buyer/vendor list with top-5 exposure %

- 60–90 days order pipeline documented

- Short “Use of Funds” note + repayment plan

- Consent-ready—know what you’ll share and why

Final Thought

If you remember just one line, make it this: In MSME lending, data is the new collateral and trust is the new interest rate.

Build your data credibility, demand explainability, and embrace tools that make credit fairer and faster. That’s how we turn small businesses into strong businesses.

Tell me one thing you’ll fix this week (bounces, MIS, GST on time, buyer concentration?). Comment below.

Learn more about how I can support your MSME journey: smartcreditwithsangeeta.com